This event serves as a premier platform for industry leaders, stakeholders, and experts to converge and discuss pressing issues and opportunities in the coal, iron ore, pellet, direct reduced iron (DRI), ferrous scrap and steel sectors. With India and China, two of the world’s largest developing economies and coal consumers, navigating energy transition challenges, the conference will delve into ‘multiple energy pathways’ aimed at mitigating carbon emissions while maintaining coal’s crucial role in the energy mix until at least 2040. Discussions will encompass regional supply-demand dynamics, advancements in carbon capture technologies, and the regulatory landscape, providing attendees with invaluable insights into shaping the future of these industries.

Simultaneously, the event is dedicated to exploring core challenges and opportunities within India’ s iron ore and pellet industry.With a focus on demand supply dynamics, policy transformations, and India’ s journey towards decarbonization, attendees can expect insightful discussions on global iron ore market trends, future trajectory of imports and prices, and the consequential impacts on the industry.

The event will address the growing DRI industry in India, driven by rising demand for sponge iron as a steel production raw material & will also delve into the potential export opportunities.Furthermore, it will explore evolving dynamics in the global scrap market and import opportunities for Indian mills.

This summit is meticulously designed to navigate through the dynamic landscape of demand-supply dynamics, policy transformations, and their consequential impacts on the market. Moreover, it aims to scrutinize India’s journey towards decarbonization while oering insightful discussions on global ion ore market dynamics.

Anticipated discussions will revolve around the future trajectory of iron ore and pellet production, imports, exports and prices, providing attendees with a comprehensive outlook on the industry’ s direction.

Steel has been a critical component of India’s economic growth, with the steel industry accounting for a significant portion of the country’s GDP. The future expansion of the Indian steel industry looks promising, with increasing demand for steel in infrastructure development, automotive manufacturing, and construction.

Additionally, the Direct Reduced Iron(DRI) capacity in India is also growing.India’ s DRI industry is set to grow at a 6 % CAGR by 2030, with annual forecasted production ranging from 65 to 70 million tonnes by FY’ 30. With the expansion of DRI capacity and improved production techniques, India is well positioned to tap the potential export opportunities.

Furthermore, the global scrap market is constantly evolving driven by factors such as geo-political conditions, trade policies and environmental regulations. This presents new opportunities for Indian mills to import scrap from various sources. India’s increasing steel scrap imports highlight the country’s potential to become a major player in the global steel industry and further boost its economic growth.

The world’s largest developing economies and coal consumers, India and China, are currently navigating energy transition challenges by adopting ‘multiple energy pathways’ to mitigate carbon emissions, rather than opting for a complete coal phase-out.

India, as one of the fastest - growing economies globally, asserts that coal will remain a crucial energy source until at least 2040, serving as an affordable energy option with demand yet to peak.In this context government authorities have consistently underscored the importance of coal.

If you attended previous conferences and want to participate in the programme again, then please hurry and get your Download Participants List!

Download Participants ListThis session will spotlight the growth trajectory of the Indian steel industry, analyzing key macroeconomic factors and its significant contribution to India 's GDP.

This session will spotlight the forthcoming steel capacity expansion strategies of Indian mills, alongside strategic mapping of India's projected raw material demands for steel production by 2030, covering resources such as iron ore, coal, scrap, and DRI, and logistics efficiency improvements, emphasizing their pivotal roles in driving future demand growth.

This session will delve into the exploration of incremental supplies from India's key states and outlook on imports.

This session will focus on exploring government policies and potential transformations in coking coal supplies to India.

This session will focus on Assessing technological advancements such as DR grade vs BF grade pellets and identifying opportunities for capacity expansion and future of Indian merchant pellet players.

This session will delve into Analysis of Mongolia's coking coal reserves and their potential for meeting India's demand.

Actor | Poet | Author | Singer

This session will focus on exploring innovative strategies and technologies to achieve decarbonization in the steel industry.

This session will delve into mining regulations and government Policies on mineral exploration, status of NMI & creation of iron ore exchange.

This session delve into addressing supply concerns, price viability issues and prospect of rising met coke imports.

This session will delve on the dynamic factors and market forces shaping the pricing trends of raw materials and steel.

This session will have discussions on examination of current trends, impact of geopolitical factors and future projections for bulk vessel freight markets.

Iron Ore Beneficition for DRI & Pelletisation, Dry Benefication of Coal for DRI & power Plant Techno-Commercial advantages of Iron Ore Benefication and Dry Benefication of Coal.

Indian DRI capacity is expected to expand in the coming years, driven by increasing demand for steel in the country.This session will focus on the opportunities and challenges in this sector,as well as the strategies for Indian DRI producers to capitalize on the growing market demand.

This session will focus on India's efforts towards reducing its reliance on thermal coal imports by improving domestic coal production.

This session will focus on the constantly evolving global scrap market driven by factors such as geo - political conditions, trade policies and environmental regulations.This presents new opportunities for Indian mills to import scrap from various sources around the world.

General Manager, India & Sub-Continent Region

C & D Steel International, India

Sr. Divisional Head (Strategic Procurement & DRI Sales)

Tata Steel Long Products Limited

Sr. Director - Consulting Business Development & Service India

South East Asia, Sphera, India

If you want to attend this conference and participate in the programme, then please hurry and register now!

Register Now

16-August-2024

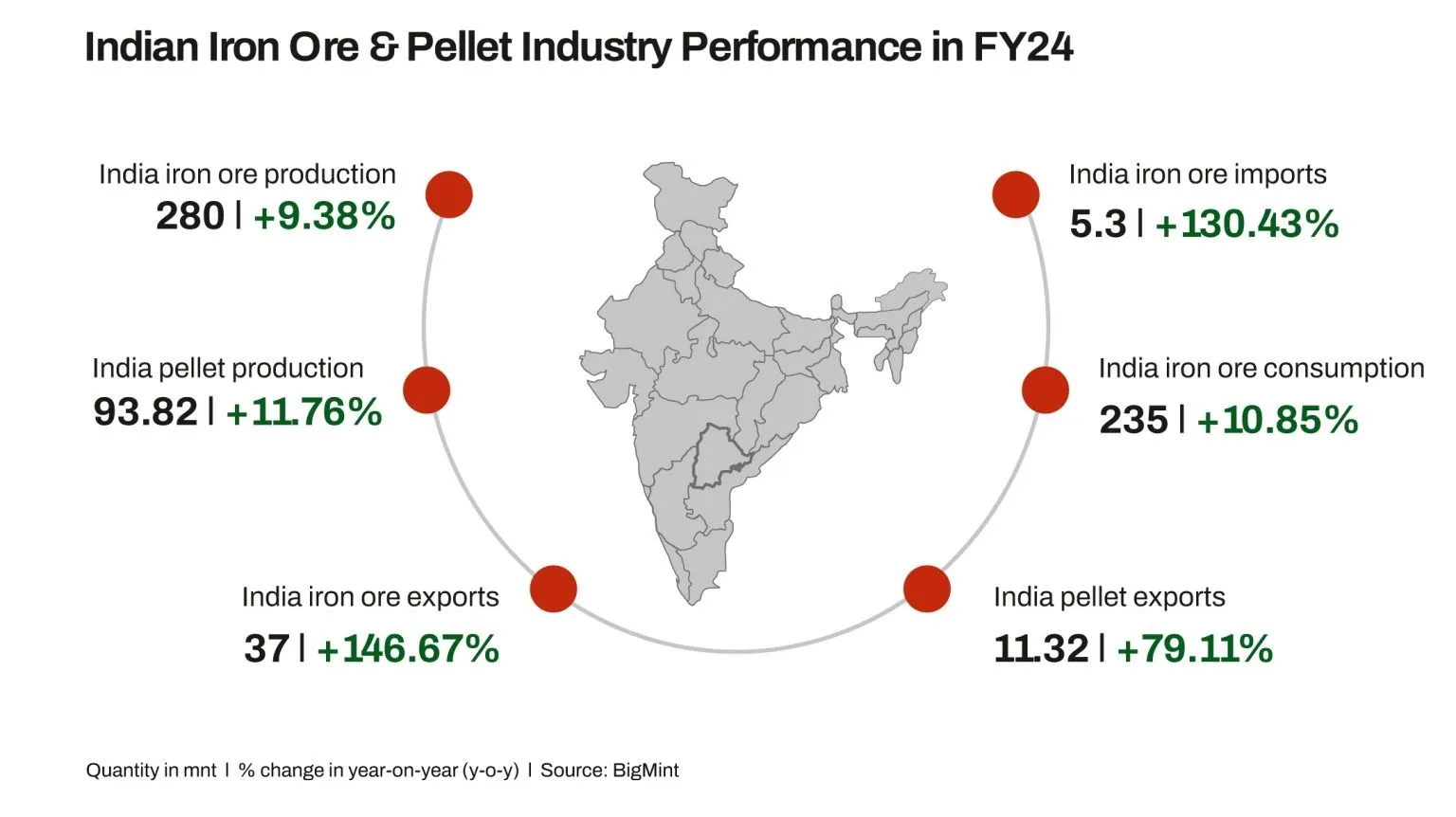

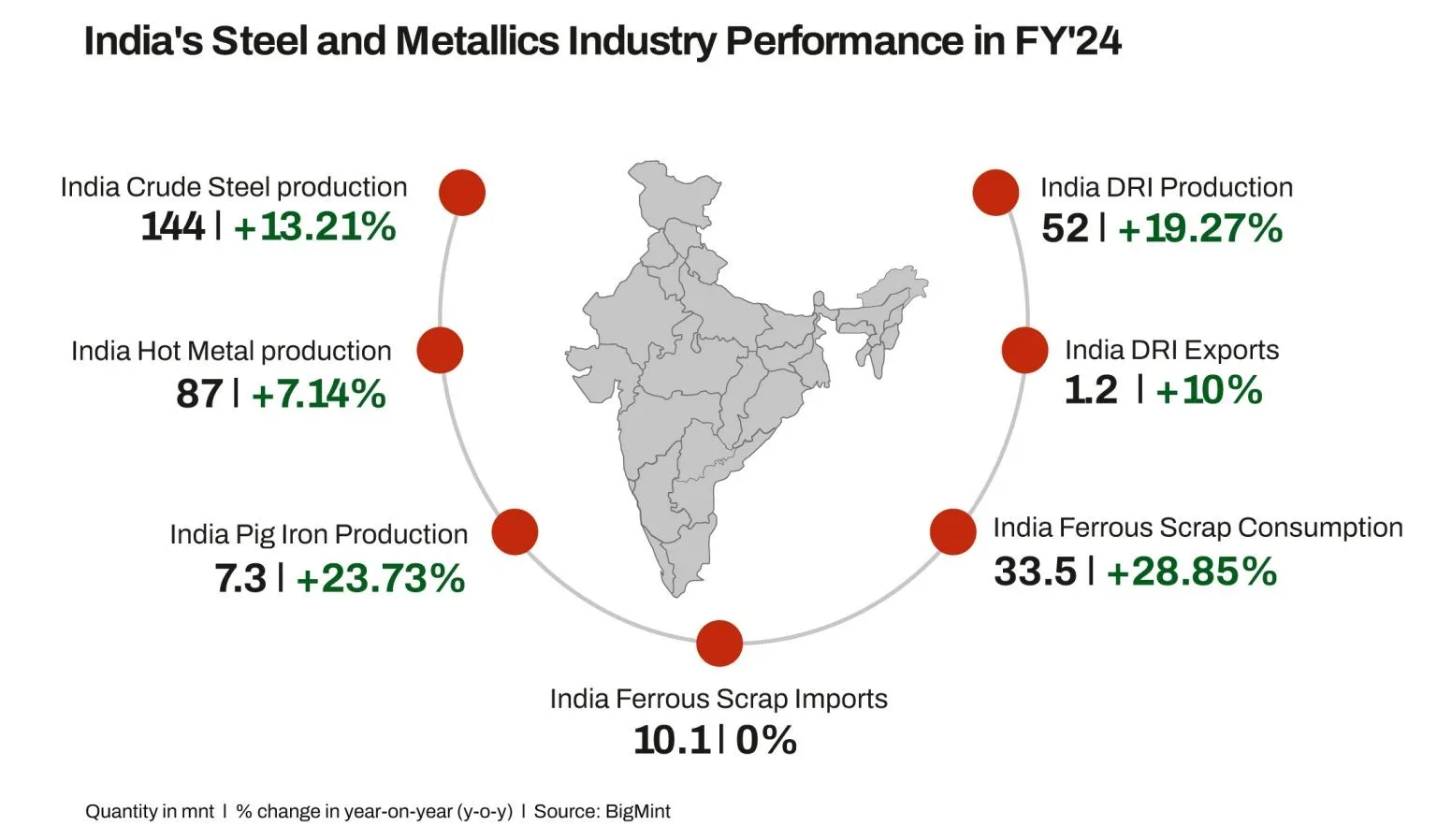

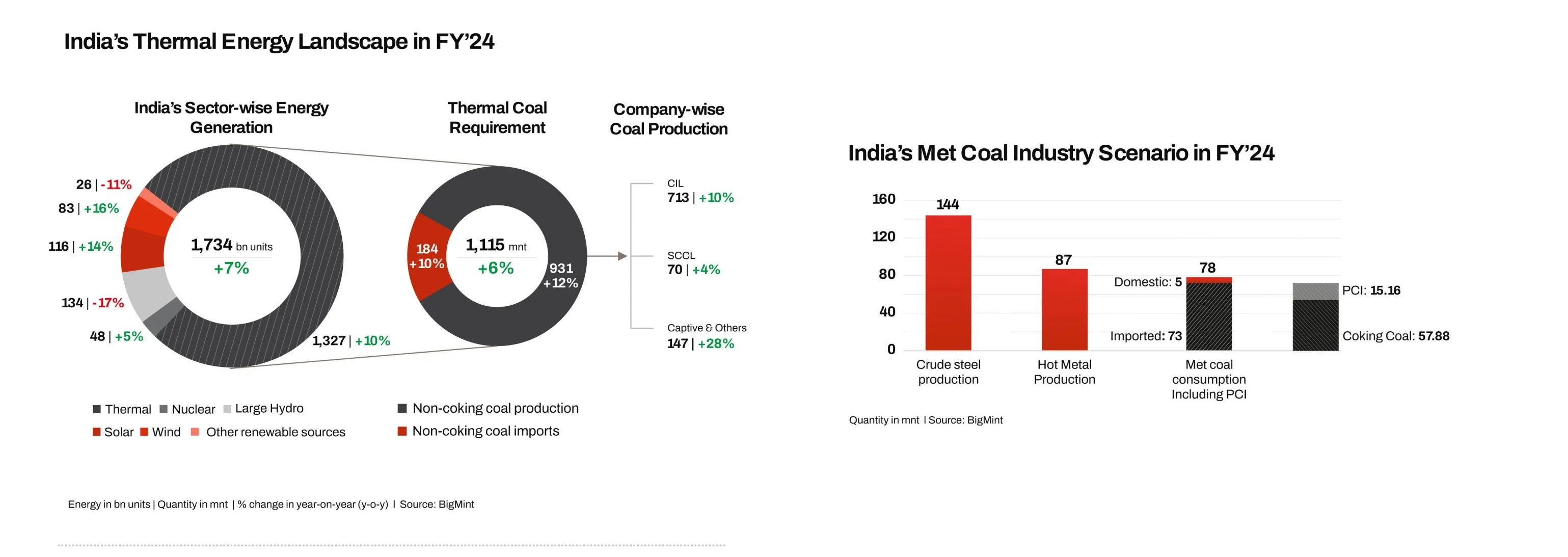

Rise in India's crude steel production: India's crude steel production increased 13% y-o-y in FY'24 to 144 mnt against 127 mnt in FY'23. The growth was propelled by a sharp increase in the share of production through the induction furnace (IF) route, which uses sponge iron as a key raw material for iron-making. As a result, DRI share in the hot metal mix rose 16% in FY'24 to 50 mnt compared to 43 mnt in FY'23.

16-june-2024

India's ferrous scrap imports are likely to see a significant over 30% decline to ~7 million tonnes (mnt) in financial year 2024-25 (FY'25) compared to 10 mnt in the previous fiscal, as per BigMint's analysis.

14-June-2024

India's imports of metallurgical coal in January-May 2024 (5MCY'24) stood at 31.7 million tonnes (mnt), an increase of 9% y-o-y compared with 29.1 mnt in 5MCY'23 as per BigMint data, on higher crude steel and hot metal production.

12-June-2024

Global seaborne metallurgical coke export volumes decreased around 5% y-o-y to 27 million tonnes (mnt) in 2023 from around 28.5 mnt in 2022, as per provisional data available with BigMint.

10-June-2024

India's imports of non-coking coal, largely used in power generation as well as other industrial applications, increased by 12% y-o-y to nearly 80 million tonnes (mnt) in January-May 2024 compared to a little over 71 mnt in the same period of last year, as per data collated by BigMint.

Mr. Ajeet Singh

+91 90092 22344

ajeet@bigmint.co

Mr. Faizan Raza

+91 95751 00430

faizan@bigmint.co

Ms. Vinamrata Jaisinghani

+91 62637 51163

vinamrata@bigmint.co